Acquiring and applying financial knowledge daily is important and beneficial for leading a better life. However, knowing why some individuals are good savers while others need help to keep money for a week is a different problem. Psychological factors are a major determinant of it, including attitude and mood, personality characteristics, and cognitive preconditions. With this, here are some of the major psychological factors affecting the learning and use of finances :

:

1. Mindset and Financial Literacy

A growth mindset posits that a person’s skills are not fixed and hence can be achieved through practice, pushing a person to continue seeking more information about finances. On the other hand, those with a fixed mindset might think that the ability to handle money is something they lack innately and, therefore, avoid competency-building experiences. When people are locked into a fixed mindset, they are unlikely to want to work hard and change bad spending habits when exposed to financial education.

2. Self-Efficacy and Confidence in Financial Decisions

Self-efficacy is the belief that one can be proficient at something in a specific situation, impacting confidence in financial decisions. High self-efficacy points to confidence in managing one’s economic life. On the other hand, people with low financial self-efficacy are likely to feel overwhelmed and hence avoid any situation involving undertaking a financial task or decision-making.

3. Emotions and Financial Decision-Making

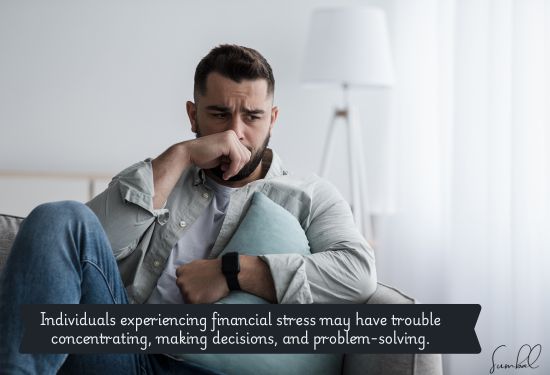

Hence, emotions such as fear, anxiety, and even excitement can act as strong drivers when handling money. For example, the financial stress arising from debt or the unknown can significantly limit a person’s capacity to learn and apply financial literacy. Since anxiety results in avoidance, it can result in people neglecting important financial activities, including budgeting or investment. On the other hand, feelings like enthusiasm and curiosity will help a lot in learning since individuals will feel interested in the same.

4. Cognitive Biases and Their Influence on Financial Learning

Cognitive biases, which are systematic distortions from the norm or rationality in judgment, are evident in financial learning and application. One type is overconfidence bias, which is when a person overestimates their knowledge or expertise. The problem with overconfidence is that it self-reinforces and can cause bad financial choices due to foregone new information. Similarly, confirmation bias, which entails seeking information that supports a given decision, also prejudices the process of financial learning. Stepping into another alternative platform narrows the flexibility of thinking in a new way or eradicating a wrong perception, which is vital in decision-making.

5. Personality Traits and Financial Behavior

There are personality characteristics that have been associated with financial behaviors. For instance, it is expected that those with high conscientiousness will be more hard-working, ordered, and responsible and thus will take a step to find out how to manage their little money. Those with a low level of self-control, a high level of impulsiveness, or low conscientiousness may need more discipline to apply financial knowledge, failing in areas such as following a budget or being able to wait for the desired financial reward.